What Is the Private Markets Liquidity Problem in Australia?

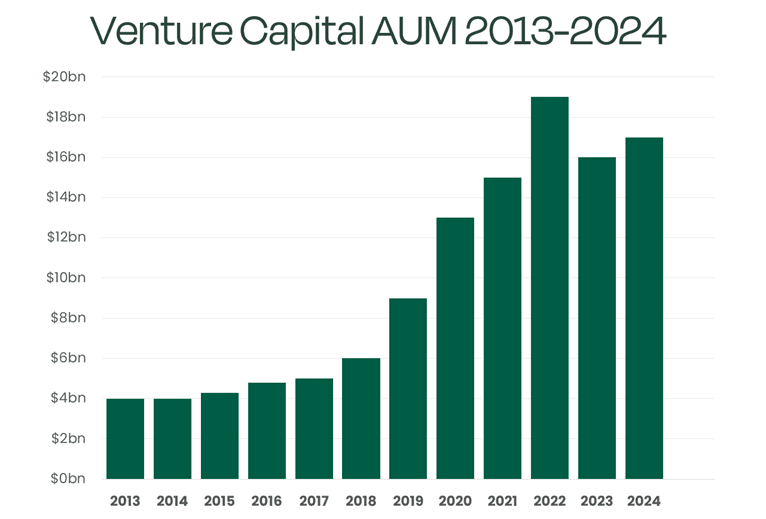

Australia’s private markets have grown significantly over the past decade, but the infrastructure to support liquidity within those markets has not kept pace. Venture capital assets under management (AUM) in Australia grew from approximately $4 billion to $17 billion between 2013 and 2024 – with a peak at ~$19 billion in 2022 according to the Australian Investment Council and Preqin’s Australian Private Capital 2025 Yearbook, a meaningful expansion of committed private capital.

But the exit market, the mechanism through which founders, employees, and investors realise the value of that capital, has moved in the opposite direction.

A recent LinkedIn post from Lak Anath highlighted the global dimension of this problem: global venture capital AUM have grown from approximately $200 billion in 2005 to over $3 trillion today – and roughly 32,000 venture-backed companies sit in a global exit backlog. The Australian data tells a comparable story, and it deserves its own examination – see below.

What Has Happened to ASX IPO Listings in Recent Years?

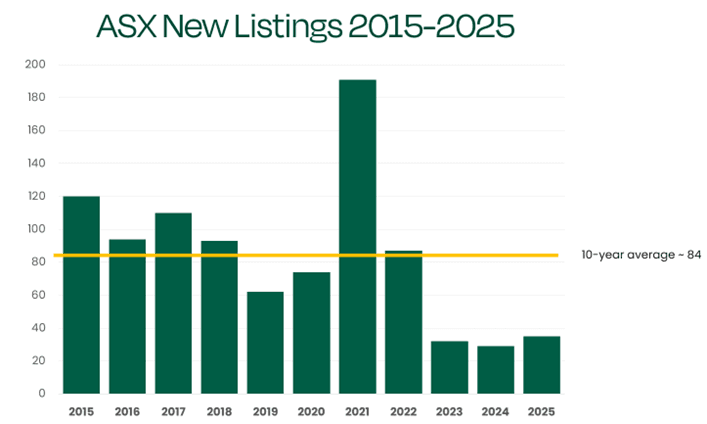

The IPO has historically been the primary exit pathway for venture-backed and private equity-backed companies in Australia. That pathway has narrowed considerably – according to HLB Mann Judd’s independent IPO Watch Australia Report, which excludes dual listings, backdoor listings, and secondary listings with no new capital raised, ASX listing activity over the past three years has been as follows:

- 2023: 32 new ASX listings

(Source: HLB Mann Judd IPO Watch Australia Report 2024) - 2024: 29 new ASX listings, the lowest level of activity in over two decades

(Source: HLB Mann Judd IPO Watch Australia Report 2025) - 2025: 35 new ASX listings

(Source: HLB Mann Judd IPO Watch Australia Report 2026)

These numbers show significant drop-off compared to the 10-year average of approximately 84 new listings per year – showing that the IPO window is no longer a reliable exit pathway for Australian companies. This is precisely the environment in which FCX’s regulated secondary market infrastructure becomes necessary.

Is Australia’s Private Markets Liquidity Problem Structural or Cyclical?

The subdued IPO environment is partly a product of elevated interest rates, post-pandemic valuation resets, and macroeconomic uncertainty. But these cyclical factors hide a deeper structural reality: Australia built its capital markets framework for a listed-markets economy, and private capital has outgrown that framework. The regulatory architecture, the exit infrastructure, and the intermediary ecosystem were all designed around the assumption that high-growth companies would eventually list. Many no longer need to.

The Australian Securities Exchange was designed to serve publicly listed companies. It was not built to absorb the growing volume of private capital that now requires a pathway to realise value. The consequence is a widening gap between committed capital and realisable value across the Australian private markets ecosystem.

FCX was established to close that gap, operating under a Tier 2 Australian Market Licence and a Clearing and Settlement Facility Licence, both issued by ASIC and the RBA.

ASIC Chair Joe Longo identified this dynamic directly in his keynote address at the National Press Club in November 2025, noting that the rapid growth of private capital is enabling companies to stay private for longer, and that “new platforms entering the Australian market, including FCX, are building new bridges between public and private markets”. Longo also cautioned that private market growth carries risk – particularly when private markets operate without adequate transparency or regulatory oversight. That is a real challenge, and it reinforces the case for regulated infrastructure rather than unregulated workarounds.

Who Is Affected by the Australian Private Markets Liquidity Gap?

The private markets liquidity gap affects multiple groups of stakeholders across the Australian innovation and investment ecosystem:

- Founders and early investors face extended holding periods with no regulated mechanism to offer liquidity, even where the underlying business is performing strongly

- Employees with equity holding options or shares under Employee Share Ownership Plans (ESOPs) have no clear pathway to realise their equity, which directly affects talent attraction, retention, and company culture

- Cap table complexity increases over successive capital rounds, creating governance challenges and making future transactions more difficult to execute efficiently

- Wholesale and institutional investors seeking exposure to private markets have limited visibility and limited ability to manage liquidity within those positions

These are not hypothetical problems. They compound over time, slowly weakening the incentive structures that underpin Australia’s innovation economy. Addressing them requires regulated market infrastructure purpose-built for private capital – not a repurposing of public market tools.

What Is a Secondary Transaction in Private Markets?

A secondary transaction is a sale of existing shares from one holder to another. No new capital is raised and no new shares are issued. The company’s ownership changes hands, but its balance sheet doesn’t. Every trade on the ASX is a secondary transaction, and in listed markets the whole process is unremarkable: transparent pricing, standardised settlement, legal certainty on both sides.

In private markets, none of that infrastructure exists by default. Without a regulated platform sitting in the middle, secondary transactions tend to happen ad hoc and often without the company’s knowledge. A shareholder finds a buyer through a broker, a bulletin board, or a personal introduction. They agree a price between themselves. Settlement means a manual update to the share register, and the company may only find out when a name it doesn’t recognise appears on the cap table. That creates real problems: governance gaps, valuation uncertainty, and potential compliance exposure for directors under the Corporations Act.

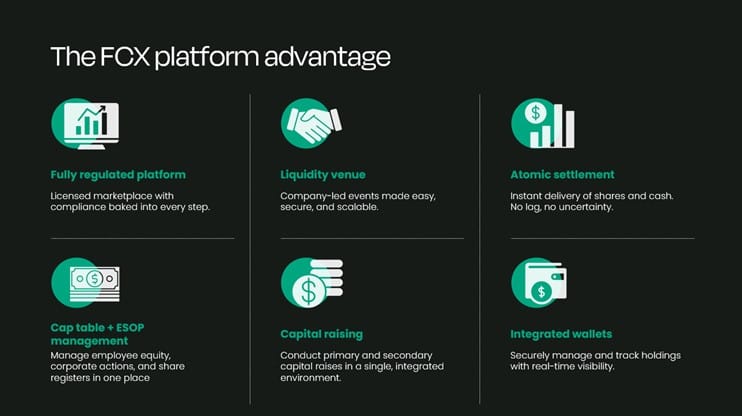

What Is FCX and How Does It Address the Private Markets Liquidity Gap?

FCX is Australia’s only ASIC and RBA regulated private market platform with both a Market Licence and a Clearing and Settlement Facility Licence. FCX provides private companies with a structured, compliant, and transparent pathway to offer liquidity in an illiquid market, through secondary transactions, tender events, and ESOP liquidity programmes, without requiring a public listing.

FCX is 100% owned by FinClear, Australia’s leading independent market infrastructure provider, which supports approximately 1.4 million investor accounts and clears approximately $360 billion in listed equities annually. Through FinClear’s network of over 250 AFSL clients, brokers, and wealth platforms, FCX provides private companies with access to genuine buy-side distribution for their liquidity events.

Transactions executed on the FCX platform are settled with atomic finality using distributed ledger technology, creating a complete and immutable audit trail. This brings listed-market rigour to private market transactions, giving companies, investors, and employees confidence in the process and its outcomes.

What Does the Future of Australian Private Markets Look Like?

The development of a mature secondary market infrastructure in Australia is both an economic necessity and a strategic opportunity. Markets with well-developed secondary transaction frameworks have demonstrated that reliable liquidity mechanisms enhance the attractiveness of private investment. Investors commit capital more confidently. Founders attract and retain talent more effectively. And the broader innovation ecosystem benefits from capital recycling more efficiently between generations of companies.

Australia is at an early but important inflection point in this development. The regulatory framework and the licensed market infrastructure exists while the demand from founders, investors, and employees continues to grow. The private markets liquidity gap is a structural problem, and it will require structural solutions.

The trajectory is clear: within the next five years, secondary transactions in Australian private markets should move to being the norm. We expect the companies that adopt regulated liquidity infrastructure early will attract better talent, access deeper pools of capital, and build the governance frameworks that position them for eventual public market participation – or for remaining private on their own terms. Australia has the regulatory framework and the licensed infrastructure to lead this transition. The question is no longer whether private markets need liquidity solutions, but how quickly the ecosystem will adopt them.

Get in Touch

If you would like to understand how FCX can support your company’s liquidity strategy, get in touch with the FCX team at contact@fcx.com.au

Sources

- ASX Media Release 2015

- IPO-WATCH-REPORT-2017-FINAL.pdf

- Australian IPO Report 2018 – HLB Mann Judd

- HLB Mann Judd’s IPO Watch Report 2019 | HLB Mann Judd

- 2021 IPO Watch Australia Report – HLB Mann Judd

- IPO Watch Australia | 2022 Report | HLB Mann Judd

- 2023 IPO Watch Australia Report – HLB Mann Judd

- 2024 IPO Watch Australia Report – HLB Mann Judd

- 2025 IPO Watch Australia Report – HLB Mann Judd

- HLB Mann Judd IPO Watch Australia Report 2026

- Australian Investment Council / Preqin Australian Private Capital 2025 Yearbook – Investmentcouncil.com.au

- ASIC Chair Joe Longo, National Press Club Keynote Address, November 2025

- Linkedin Post from Lak Anath, April 2026